Key Takeaway

GST Eliminates Cascading Taxes: By unifying multiple taxes into a single system, GST reduces the cascading effect of taxes, lowering the overall tax burden on consumers.

GST Simplifies Compliance: The introduction of systems like the GST Network (GSTN) simplifies the process of tax filing and increases transparency, making compliance easier for businesses.

GST Enhances Inter-State Trade: The implementation of IGST facilitates smoother inter-state transactions, promoting a more unified national market.

GST Supports Small Businesses: With mechanisms like the Composition Scheme, GST supports small businesses by simplifying compliance and reducing tax liabilities.

GST Adjusts to Economic Feedback: Ongoing adjustments to GST rates and policies reflect the system’s adaptability to economic conditions and stakeholder feedback, aiming for fairness and efficiency.

The Journey of GST in India

The implementation of the Goods and Services Tax (GST) in India marked a transformative leap in the country’s fiscal framework, simplifying a complex and fragmented tax system into a more transparent, cohesive, and streamlined model. This journey began long before the actual implementation date on July 1, 2017.

The idea of a unified goods and services tax had been a topic of discussion in Indian economic policy circles for decades, but concrete steps towards this vision started in 2000 when the then-Prime Minister Atal Bihari Vajpayee set up a committee to draft the GST law. Over the next 17 years, the proposal went through extensive consultations and revisions, involving stakeholders across the board, including state governments, the central government, and various industry leaders, to address numerous political and economic concerns.

One of the major challenges was the apprehension of state governments about losing their autonomy over tax revenue, which was addressed by promising full compensation for any revenue loss for the first five years of GST implementation. Another challenge was the technological requirement for managing such a comprehensive tax system, which led to the establishment of the GST Network (GSTN), a sophisticated and robust IT backbone that ensured the successful management and facilitation of the new tax regime.

Finally, after much deliberation, the Constitution (One Hundred and First Amendment) Act, 2016, set the stage for the introduction of GST, which was launched in a historic midnight session of Parliament on July 1, 2017. This new tax regime subsumed nearly all indirect taxes at the central and state levels into a single tax, thereby eliminating the cascading effect of taxes and paving the way for a common national market.

Since its inception, GST has undergone several rounds of revisions to rates and policies to accommodate the practical challenges faced by businesses and to respond to the feedback from various sectors of the economy. These revisions have been aimed at optimizing the tax structure, making it fairer, simpler, and more revenue-neutral for all stakeholders involved.

The journey of GST in India is a continuing process of refinement and enhancement as it adapts to economic dynamics and seeks to fulfill its role as a catalyst for economic growth and simplification of the tax system.

Objectives of GST

The introduction of the Goods and Services Tax (GST) in India was driven by several key objectives aimed at enhancing the efficiency of the tax system and boosting the economy:

- To Eliminate the Cascading Effect of Taxes: GST was designed to remove the cascading effect of taxes, where taxes were previously imposed on an already taxed amount, leading to higher overall tax burdens on the end consumer.

- To Simplify the Tax Structure: By consolidating multiple central and state taxes into a single tax, GST simplifies the tax structure, making it easier for businesses to comply and reducing the complexities associated with managing various indirect taxes.

- To Increase Compliance: GST’s streamlined process and infrastructure, such as the GST Network (GSTN), encourage better compliance due to its simplified and transparent system.

- To Broaden the Tax Base: With its structured compliance and simplified regulations, GST broadens the tax base by bringing more businesses under its purview and minimizing tax evasion.

- To Enhance Revenue Efficiency: GST is intended to increase tax revenues by improving the efficiency of tax administration and ensuring better compliance.

- To Promote Cooperative Federalism: GST fosters cooperative federalism by involving both the Central and State governments in the sharing of resources and responsibilities related to indirect taxation.

Advantages of GST

The implementation of GST brings numerous advantages to the Indian economy, businesses, and the general public:

- Removal of Multiple Indirect Taxes: GST replaces various taxes like VAT, Excise Duty, Service Tax, and several other indirect taxes, thereby simplifying the tax structure.

- Prevention of Tax-on-Tax: Earlier, the input taxes paid could not be fully credited, which led to a cascading effect. GST avoids this by ensuring that tax is paid only on the value addition at each stage of the supply chain.

- Increased Ease of Doing Business: By harmonizing the indirect tax structure, GST has reduced the complexities involved in intra-state and inter-state movement and sale of goods. This change has been instrumental in facilitating smoother logistics and faster delivery services.

- Boost to the ‘Make in India’ Initiative: By providing a boost to domestic manufacturing and making products competitive in national and international markets, GST aligns with the ‘Make in India‘ initiative.

- Improved Tax Compliance and Revenue Collections: With an organized system of tax filing through digital platforms and regular updates, GST ensures better compliance, leading to increased revenue collection for governments.

- Enhanced Efficiency in Logistics: Reduction in transit times and costs as the need for warehouse optimization has decreased due to the removal of inter-state check posts.

- Fair Pricing for Consumers: As businesses benefit from input tax credits and reduced tax burdens, the benefits are often passed on to consumers in the form of lower prices.

By addressing the inefficiencies of the previous tax system and integrating the Indian market into a single tax regime, GST has played a crucial role in shaping a more stable and predictable taxation environment in India.

💡If you want to pay your GST with Credit Card, then download Pice Business Payment App. Pice is the one stop app for all paying all your business expenses.

The Structure or Framework of GST in India

The Goods and Services Tax (GST) in India features a dual structure designed to be comprehensive and integrated across the country, ensuring both central and state governments can levy and collect taxes. This system is called the dual GST model, which includes Central GST, State GST, and Integrated GST, alongside a specific variant for Union Territories.

What is SGST?

State Goods and Services Tax (SGST) is a component of the Goods and Services Tax (GST) implemented in India, which is levied and collected by individual state governments on intra-state sales of goods and services. This means that whenever a transaction occurs within a single state, SGST is applied in addition to the Central Goods and Services Tax (CGST). The revenue collected under SGST is exclusively for the state where the transaction occurs, helping to fund various state-specific projects and services. Each state has its own SGST Act, which details the regulations and procedures related to SGST administration within that state.

What is CGST?

Central Goods and Services Tax (CGST) is the portion of GST that is levied by the Central Government on intra-state supplies of goods and services. Like SGST, CGST is applied to all transactions occurring within a state but the revenue generated from CGST goes directly to the central government. It is charged at the same rate as SGST, and the two are applied simultaneously on the same base, ensuring that the total tax rate is split between the state and central governments. This structure helps maintain a balance between the financial autonomy and policy prerogatives of both levels of government.

What is UTGST?

Union Territory Goods and Services Tax (UTGST) is the tax levied by the Union government on transactions of goods and services taking place within the boundaries of India’s Union Territories that do not have their own legislature. This includes Union Territories like Chandigarh, Andaman and Nicobar Islands, Lakshadweep, Daman and Diu, and Dadra and Nagar Haveli. UTGST is structured similarly to the State Goods and Services Tax (SGST), applying in parallel with the Central Goods and Services Tax (CGST) on intra-union territory transactions. The revenue collected from UTGST goes to the Union Territory administration, helping to fund local infrastructure and services.

What is IGST?

Integrated Goods and Services Tax (IGST) is charged on all inter-state transactions of goods and services, as well as on imports into India. It is governed by the IGST Act, which is a component of the overall GST laws in India. The IGST mechanism is designed to ensure that the tax is collected by the central government but shared between the originating (supplying) state and the consuming (destination) state. This tax ensures that the state which consumes the goods or services accrues the revenue from the GST. IGST simplifies tax collection on inter-state purchases, reducing the need for separate state-level compliance and facilitating a smoother mechanism for monitoring and transferring tax revenues between states.

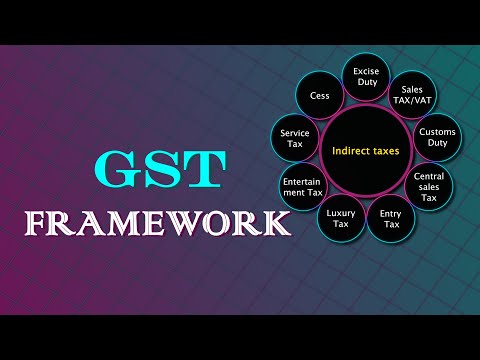

Tax Laws Before GST

Before the introduction of the Goods and Services Tax (GST) in India, the tax system was fragmented with a multitude of complex, overlapping indirect taxes levied by both state and central governments. Key components of this system included:

- Value Added Tax (VAT): Levied by state governments on the sale of goods within their territories, with rates varying from state to state.

- Central Excise Duty: Imposed by the Central Government on the manufacture of goods within the country.

- Service Tax: Charged by the Central Government on the provision of services.

- Additional Customs Duty: Also known as Countervailing Duty (CVD), it mirrored the Central Excise Duty and was levied on imported goods to align the tax burden of imported and domestically produced goods.

- Special Additional Duty of Customs (SAD): Levied to counterbalance sales tax, VAT, and other local taxes previously imposed on imported goods.

- Entry Tax: Collected by State Governments for the movement of goods from one state to another.

- Luxury Tax, Entertainment Tax, etc.: Imposed by state governments on the consumption of various services and luxury products.

These multiple taxes created a complex tax environment leading to the cascading effect of taxes, where tax was paid on a tax, increasing the overall burden on the final consumer.

What are the GST Tax Rates in India?

GST in India is structured around four primary tax rate slabs, aimed at providing a progressive tax structure that helps in reducing the tax burden on essential items while collecting higher revenues from luxury items. The current GST tax slabs are:

- 5%: This lower rate is applicable on essential commodities such as packaged food items, clothing, etc.

- 12%: A standard rate applied to goods and services that include daily use items.

- 18%: This higher standard rate is levied on goods and services like electronic goods, mobile phones, restaurant services, etc.

- 28%: Applied to luxury items and certain demerit goods like aerated drinks, luxury cars, and certain tobacco products. Certain items in this category also attract a cess in addition to the 28% GST, known as the GST Compensation Cess, intended to compensate states for any revenue loss due to the implementation of GST.

This streamlined structure aims to simplify the tax system, broaden the tax base, and reduce economic distortions caused by tax on tax effects prevalent in the pre-GST regime.

Who is Required to Register Under GST?

Registration under the Goods and Services Tax (GST) in India is mandatory for businesses whose turnover exceeds the following thresholds:

- Rs 40 lakhs for suppliers of goods in most states.

- Rs 20 lakhs for suppliers of goods in special category states (Northeastern states, Himachal Pradesh, Uttarakhand, and Jammu & Kashmir).

- Rs 20 lakhs for suppliers of services in most states.

- Rs 10 lakhs for suppliers of services in special category states.

Additionally, certain other criteria also mandate GST registration, irrespective of turnover:

- Businesses involved in inter-state supply of goods and services.

- Taxable persons supplying goods on behalf of other taxable persons (agents and brokers).

- Providers of online information and database access or retrieval services from a place outside India to a person in India, other than a registered taxable person.

The GST regime mandates that every eligible business must register in each state or union territory from where they operate or supply goods or services. This registration ensures compliance with tax laws and enables businesses to claim input tax credit.

What is the GST Compensation Cess?

The GST Compensation Cess is an additional levy on certain goods and services over and above the GST rates, designed specifically to compensate states for any loss of revenue due to the implementation of GST. This cess was introduced as part of the GST laws to ensure that states do not face financial losses in the first five years of GST implementation from July 1, 2017.

The cess applies primarily to luxury and demerit goods such as high-end cars, tobacco products, and aerated drinks. The revenue collected from this cess is used to fund the compensation paid to states, ensuring that their revenue remains stable during the transition period to the new GST system. The GST Compensation Cess is set to be in place for a period that extends up to five years from the inception of GST, unless extended further by the GST Council if states continue to need revenue support.

How Has GST Helped in Price Reduction?

The implementation of the Goods and Services Tax (GST) has contributed to price reduction in various ways, streamlining the tax structure and improving the efficiency of the supply chain across India. Here are key aspects through which GST has facilitated lower prices for consumers:

- Elimination of Cascading Tax Effects: Before GST, the tax-on-tax system meant that consumers paid tax over tax throughout the supply chain, leading to higher overall costs for goods and services. GST has eliminated these cascading effects by implementing a seamless credit system across the chain, which reduces the end-cost to the consumer.

- Improved Supply Chain Efficiency: GST has standardized the tax rates across the country, removing the complicated multiple tax structures that varied from state to state. This unification has reduced the logistical and compliance-related costs that businesses had to bear. The reduction in overhead costs for businesses has translated into lower costs for goods and services.

- Increased Competition: The transparent tax structure under GST has fostered a healthier competitive environment. Businesses are more inclined to pass on any benefits of tax savings to consumers in the form of reduced prices to attract more customers, given that the tax rates are now uniform across states.

- Boost to Manufacturing Sector: GST has also restructured the tax framework on manufactured goods by reducing the overall tax burden on manufacturers. This reduction in manufacturing costs has enabled producers to offer products at competitive prices, benefiting consumers.

- Input Tax Credit: GST allows businesses to claim input tax credit for taxes paid on raw materials, services, and other inputs. This means that the final product cost is reduced as businesses can deduct the taxes already paid at different transaction stages. This benefit is often passed on to the end consumer, resulting in lower retail prices.

Overall, while the immediate impact of GST on prices varied across different sectors, the long-term benefits have been geared towards reducing unnecessary tax burdens and promoting a more streamlined and efficient market environment, which in turn helps in keeping consumer prices in check.

FAQs

What is a GST Return and who is required to file it?

A GST Return is a document that contains details of income which a taxpayer is required to file with the tax administrative authorities. This is used by tax authorities to calculate tax liability. Every registered GST entity must file GST returns, including sales, purchases, Output GST (on sales), and Input tax credit (GST paid on purchases).

How does the E-Way Bill system work under GST?

The E-Way Bill is an electronic documentation specifically for the movement of goods, required when the value of a consignment exceeds Rs. 50,000. It can be generated on the GSTN portal and is essential for transporting goods both inter-state and intra-state, ensuring compliance with GST laws and aiding in the seamless movement of goods.

What determines if a business has to register for GST based on annual turnover?

Businesses with an annual turnover exceeding Rs. 40 lakhs (Rs. 20 lakhs for special category states) are required to register under GST. This threshold highlights the scale of business that mandates GST registration, making them liable for collecting GST on behalf of the government and filing returns.

How does GST address the issue of double taxation?

GST was designed to eliminate the problem of double taxation, or tax-on-tax, prevalent in the previous indirect tax regime. By integrating various central and state taxes into a single tax, GST ensures transparency and avoids the cascading effect of taxes, thereby reducing tax liabilities on consumers and businesses.

What is meant by aggregate turnover in the context of GST?

In GST terms, aggregate turnover refers to the total value of all taxable and non-taxable supplies, exempt supplies, and exports of goods and services of a person with the same PAN. It is calculated on an all-India basis and is used to determine GST registration and eligibility for the Composition Scheme.

What should businesses know about GST on inter-state sales?

Inter-state sales are taxable under the Integrated Goods and Services Tax (IGST), which is meant to be shared between the state where the goods are produced and the state where they are consumed. This system simplifies tax charges on goods crossing state lines, ensuring a smooth and unified market.

Who can benefit from the Composition Scheme under GST?

The Composition Scheme under GST is designed for small taxpayers to reduce compliance costs and simplify the tax process. It is available to businesses with an annual turnover of up to Rs. 1.5 crore (Rs. 75 lakhs for NE and hill states). This scheme allows qualifying businesses to pay GST at a fixed rate of their turnover and file returns quarterly, thereby easing the tax burden and simplifying the tax filing process.